Coinciding with the publication of the quarterly of the majority of the firms benefits, these days also we are seeing the output in the light of other global results as for example, the number of tablets sold in the second quarter of the year. On other occasions we have mentioned that this sector is going through a complex situation in which we observe a transition. Terminals 2 in 1 continue to increase their presence, while traditional models continue downward. In the field of smartphones, however, are facing some saturation that however, does not impact negatively on the number of units sold.

During the months from April to June, the number of tablets marketed has continued downward, showing once again, a trend which began long ago and that ended with a boom in which technology worldwide, regardless of their size, proved luck. Then you have more devices sales figures during the spring and the first part of the summer. I will also show which firms are dodging the storm, which are in a most compromising situation and finally, what could be the trend for the coming months.

The main point of

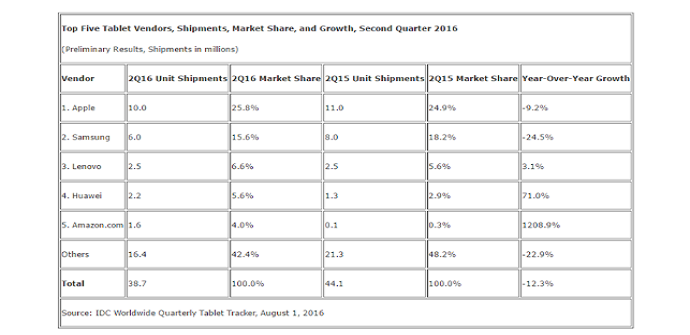

IDC, which is largely known for its statistical studies, estimated at 38.7 million tablets sold in the spring. At first glance, it may seem a good number. However, it is a 12.3% lower than in the same period in 2015, when 42 million terminal was provided. As we see, the downs have been consolidated. However, are not something circumstantial since the number of sold units reached its peak just two years ago and since then, has been declining.

Android continues to head

For operating systems, the Green robot software remains the favorite choice for those who acquire a new terminal. According to IDC, the 65% of the new acquisitions are equipped with this interface. In second place, iOS, present in 2 of every 10 tablets purchased during the spring and finally, Windows, with an approximate 10% share.

The behavior of consumers

The public is, ultimately, that decides the success or failure of a terminal. An example of how you dictate behaviour that must follow manufacturers, we see in the history of this support. In 2010 and 2011, full consolidation of the tablets, we saw how models of reduced dimensionsare demanded. During 2015 we are witnessing the rise of devices focused a more professional sector or otherwise, that may meet without problems the needs of both those who were looking for a tool for leisure, as those who sought it in the labour field. The 2 in 1 were the choice of both consumers and manufacturers. All analysts agree that at least until 2018 or 2019, we will witness a greater implementation of this last format which currently accounts for around 30% of the units sold.

Apple, leading but nuanced

As for the breakdown by brands, IDC’s show us that those of Cupertino continue to head in the second quarter. With a approximate 25% of the market share , of the bite Apple have managed to put 10 million iPads in the second quarter. However, occurred a decrease of 10% compared to the same period of 2015, when they exceeded 11 million. Samsung remains in second position although it also accused a more pronounced decrease. The Galaxy Tab are being well received, but not as much as I expected them since, as shows the next picture, firm South Korean has gone from the 8 million units sold in the spring of last year, to 6 in the same period 2016.

The Chinese firms seem to resist better the storm. Huawei is an example, since it has doubled its presence in the market thanks to models such as the Matebook, that they have served to double its share to 6 percent. At first glance, it may seem a residual fee. However, not so much if we take into account that in 2015, this era of only 2% approximately. Lenovo sale nor ill stop, since it has managed to sell 2.5 million tablets and has grown by 3% in comparison to 2015.

The future to short term

While the manufacturers are focusing is in the production of models convertible, them tablets traditional still continue dominating the sector. The celebration of them large appointments technological that remaining as the IFA, or the launch final of Android 7.0 Nougat, can be a ball of oxygen and give it turned to them data unless, of face to the campaign Christmas.

What to large features, can mean the consolidation final of a decline started makes two years, also is an opportunity for them companies at the time of innovate and offer something novel with what out of the situation in which the sector is is currently. Think that in during the next quarters, them stands convertible will be winning terrain of way more pronunciation? You think that still is margin of maneuver for the creation of tablets traditional that may be all a success of sales? You have available more information as for example, what is happening in the field of the phablets so you can check how consumer electronics is something very much alive and in which nothing is eternal.

Another fall more item: the sale of tablets low in the second quarter was published in TabletZona.